A group of U.S. Senate Democrats is challenging a major new initiative by the Federal Housing Finance Agency (FHFA), which could allow cryptocurrency holdings to play a role in mortgage approvals. The probe, led by Senator Jeff Merkley and joined by four other prominent Democrats, questions the safety, fairness, and integrity of a proposal from FHFA Director William Pulte.

Their letter, sent Friday, expresses deep concerns about the impact of including crypto assets in mortgage underwriting, a process that determines a borrower’s eligibility for a home loan.

The FHFA’s Crypto Mortgage Proposal

In June, FHFA Director William Pulte issued a directive to government-sponsored mortgage buyers Fannie Mae and Freddie Mac. The order instructed them to explore how they could factor in applicants’ cryptocurrency holdings during the risk assessment phase of single-family mortgage applications, without requiring the assets to be converted to U.S. dollars.

Currently, under federal policy, crypto is not accepted in any form during the mortgage approval process unless it is first liquidated into fiat currency. The new proposal marks a major shift in how digital assets could be recognized within the housing finance system.

Fannie Mae and Freddie Mac, both controlled by the FHFA since the 2008 financial crisis play a massive role in the U.S. housing market by purchasing and guaranteeing mortgages. Any changes to their policies could have far-reaching consequences.

Lawmakers Warn of Risks to Homeowners and the Market

The senators argue that including volatile and speculative crypto assets in mortgage evaluations could place both homebuyers and the broader financial system at serious risk.

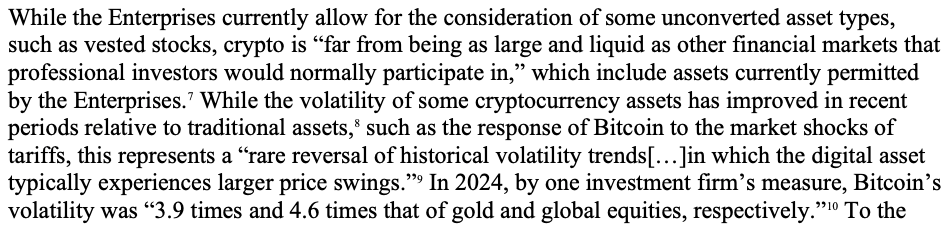

“Crypto markets have historically been prone to extreme volatility and liquidity crunches,” the senators wrote. They explained that borrowers who rely on crypto may struggle to quickly convert those assets into cash, especially during market downturns, increasing the likelihood of mortgage defaults.

They also highlighted other vulnerabilities associated with crypto, such as scams, cyberattacks, and even physical theft. These risks, they say, could leave homeowners unable to recover lost assets, a unique danger compared to traditional forms of financial collateral.

The lawmakers referred to the 2023 banking crisis, where three U.S. banks collapsed partly due to overexposure to crypto clients, as an example of how digital assets can create systemic risk if not properly regulated.

Conflict of Interest Concerns and Lack of Transparency

The senators also raised alarm about potential conflicts of interest, particularly involving Pulte himself and the Trump family.

Pulte’s spouse reportedly holds up to $2 million in crypto assets, which they say raises “serious concerns” about personal financial benefit. Moreover, Pulte, as chair of both Fannie Mae and Freddie Mac’s boards, has influence over whether and how the crypto proposal moves forward. The senators claim he has filled these boards with “industry allies,” further compromising the process.

They also pointed to potential influence from Donald Trump and his family, who are deeply tied to the crypto world through investments in platforms, mining businesses, memecoins, and NFTs.

The letter demands Pulte explain how he plans to manage or recuse himself from these conflicts of interest.

Calls for Clarity and Accountability

Beyond the ethical questions, lawmakers criticized the proposal itself as being vague and lacking essential information. They noted that Pulte’s directive included no clear timeline, methodology, or plan for assessing the risks and benefits of such a dramatic shift in mortgage policy.

Additionally, they noted past failures of the FHFA to oversee crypto-related exposure in financial institutions, warning that without a robust risk framework, the same mistakes could be repeated, this time in the housing market.

The senators asked Pulte to answer a series of questions by August 7. These include requests for internal communications regarding the crypto directive, the decision-making process that led to the order, how the agency will gather public feedback, and the steps Pulte will take to address potential conflicts.

They also reminded the FHFA of Fannie Mae’s 2021 internal research, which found that using crypto or stablecoins as deposits or collateral was the “least appealing application” of blockchain technology in the housing sector.

A Broader Debate on Crypto’s Role in the Economy

The Democratic pushback highlights a larger national debate about how cryptocurrency should be integrated into mainstream financial systems. While supporters argue that crypto offers innovation, flexibility, and a pathway to broader financial inclusion, critics warn that its speculative nature and regulatory gaps could destabilize essential institutions.

In this case, that institution is the U.S. housing market, which remains the largest source of wealth for most American families.

With a response deadline looming and growing attention from Congress, the FHFA will likely face further scrutiny in the coming weeks. Whether crypto becomes part of the mortgage process or remains sidelined due to its risks could help shape the future of both digital finance and housing access in the United States.

Leave a Reply