The European Central Bank has cautioned that the growing use of stablecoins could weaken bank lending and complicate the transmission of monetary policy across the euro area. In a newly released working paper titled “Stablecoins and Monetary Policy Transmission,” ECB staff said that rising interest in digital tokens pegged to currencies such as the US dollar and the euro may gradually draw money away from traditional bank deposits.

According to the central bank, this shift could reduce the availability of credit to households and businesses and alter how policy decisions affect the wider economy.

Deposit Shift Could Squeeze Bank Funding

The ECB’s analysis points to what it describes as a deposit substitution effect. As households and firms move funds from retail bank accounts into stablecoins, banks may see a measurable decline in deposits, which are a primary and relatively low cost source of funding.

The paper notes that deposits play a crucial role in supporting lending activities. If deposits shrink, banks could be forced to rely more heavily on wholesale or market based funding. Such funding is often more expensive and less stable, which may, in turn, restrict banks’ ability to extend credit to the real economy.

ECB researchers said their findings show a clear link between growing stablecoin adoption and a reduction in retail bank deposits, alongside a decline in lending to firms.

Implications for Monetary Policy Transmission

Beyond the impact on bank balance sheets, the report highlights broader concerns for monetary policy. The ECB said that stablecoins could interfere with several channels through which policy rate changes influence the economy.

If banks face higher or more volatile funding costs because of deposit outflows, adjustments in policy interest rates may not pass through to lending conditions in a predictable way. This could weaken the effectiveness of central bank decisions.

The authors emphasized that the effects are not uniform. The scale of stablecoin adoption, their design features and the regulatory framework surrounding them all influence the degree of impact. In some scenarios, the disruption could remain limited, but in others it could become more pronounced as usage grows.

Foreign Currency Stablecoins Raise Added Risks

The ECB also raised concerns about the dominance of foreign currency backed stablecoins, particularly those linked to the US dollar. The paper warns that when non euro denominated tokens dominate the market, the connection between domestic monetary policy and bank lending may weaken further.

ECB officials have previously voiced unease about the rise of dollar backed digital tokens and the potential implications for monetary sovereignty. A growing reliance on foreign currency stablecoins could affect the euro’s role in cross border payments and financial markets within the euro area.

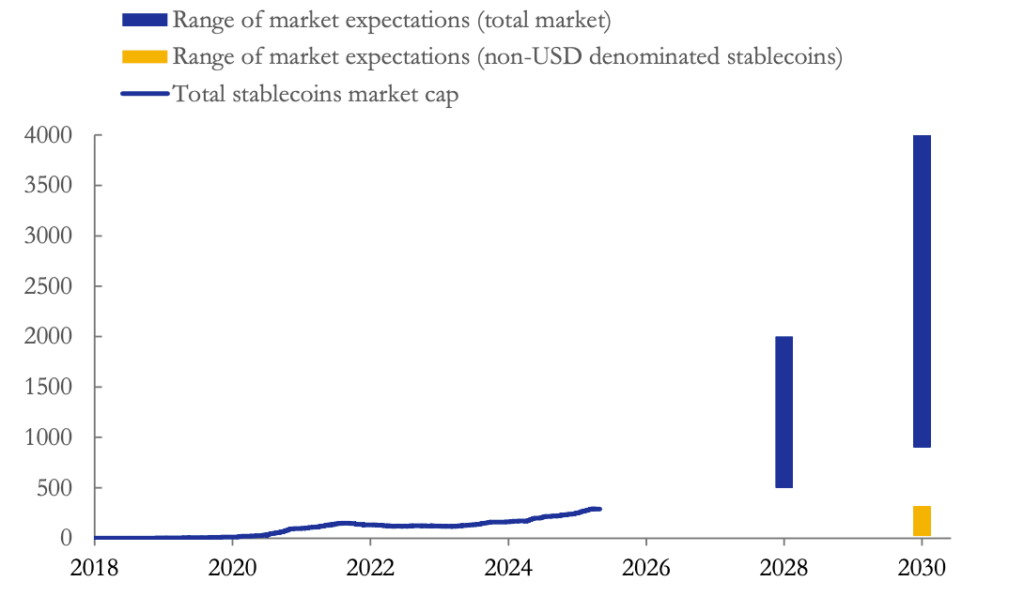

Data cited in the working paper shows that US dollar backed stablecoins account for the overwhelming majority of the market. Figures from CoinGecko indicate that dollar pegged tokens are valued at about 301 billion dollars, representing roughly 97 percent of the total stablecoin market capitalization.

Rapid Market Growth Draws Regulatory Attention

The stablecoin market has expanded rapidly in recent years. According to the ECB, the sector’s total market capitalization has more than doubled over the past three years, reaching around 312 billion dollars. Projections suggest it could grow to as much as 2 trillion dollars by 2028.

This rapid expansion has prompted regulators in Europe and elsewhere to intensify their monitoring of digital assets. The ECB said the working paper forms part of its broader effort to assess how new forms of digital money may reshape the financial system.

While stablecoins can offer benefits such as faster payments and easier cross border transfers, the central bank made clear that their growing presence also brings structural challenges. The extent of these challenges, the report concludes, will depend heavily on how stablecoins are designed and regulated as adoption accelerates.

Leave a Reply